By Paul Z. Martin, CIC, CPCU

Paul Martin is the Director of Insurance Content and Mentorship for the National Alliance for Insurance Education & Research. Paul works with industry professionals to deliver high-quality insurance content and education for the Academy. During his career, Paul worked as an adjuster, underwriter, special agent, company manager, and independent agent. Paul has been an insurance educator in Texas for over twenty years.

The Commercial General Liability (CGL) policy, courtesy of the Insurance Services Office (ISO), exhibits a comprehensive design that shields an expansive range of organizations and individuals.

A look into the ‘Who Is An Insured‘ category under Section II sheds light on the versatility of insureds semantics. This segment illustrates who qualifies as an insured automatically, marked often by the nature of the entity declared as the Named Insured.

For instance, executive officers and directors are immediate insureds if a corporation stands as the Named Insured. If the Named Insured is an individual, say an unincorporated sole proprietor, their spouse attains insured status, restricted to conduct pertinent only to the business owned exclusively by the Named Insured. Furthermore, two key insured categories– volunteers and employees–garner recognition in the CGL description.

Navigating the CGL Language and Definitions

The introductory language of the CGL coverage form states, “Throughout this policy, the words ‘you’ and ‘your’ refer to the Named Insured shown in the Declarations…” Further ahead, it defines, “The word ‘insured’ refers to any person or organization qualifying as such under Section II- Who is an Insured.” Considering these definitions, a noteworthy Condition in the policy surfaces–Condition #7, termed the Separation of Insureds.

The Condition states:

“Except with respect to the Limits of Insurance, and any rights or duties explicitly assigned in this Coverage Part to the first Named Insured, this insurance applies:

a. As if each Named Insured were the only Named Insured; and

b. Separately to each insured against whom a claim is made or ‘suit’ is brought.”

Unpacking the Importance of Separation of Insureds

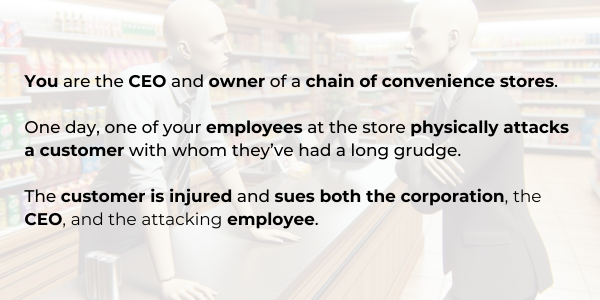

The significance of this condition may not be evident initially but consider this scenario:

This circumstance underscores the relevance of a prominent exclusion in Coverage A – the Expected or Intended Injury exclusion. This exclusion bars coverage for “Bodily injury or property damage expected or intended from the standpoint of the insured.” The usage of “the” before insured is pivotal. It disqualifies coverage for the employee but retains it for the corporation and the executive.

Despite them all being insured, “the” implies the perspective from the acting insured. The policy could have proposed “any,” “all,” or “a,” but chose “the,” confirming that each insured’s actions are separately considered.

The Separation of Insured condition has thus saved the day, since each insured is treated separately.